Pre-Foreclosures Explained: How Savvy Investors Create Instant Equity Without Buying at Auction

Learn about Pre-Foreclosures for real estate investing.

Why Pre-Foreclosures Are Misunderstood (and Profitable)

Most investors either confuse pre-foreclosures with bank-owned inventory or assume the process is too messy to touch.

That misunderstanding keeps them from the 10–30% discounts that quietly change portfolios.

When I help clients design acquisition plans, I don’t start with “find a deal.”

I start with “understand the timeline, the seller’s legal rights, and the math that protects your capital.”

I rebuilt a chunk of my portfolio in a tight credit market by focusing on this niche.

Not because I’m bold, but because the rules are clear once you learn them.

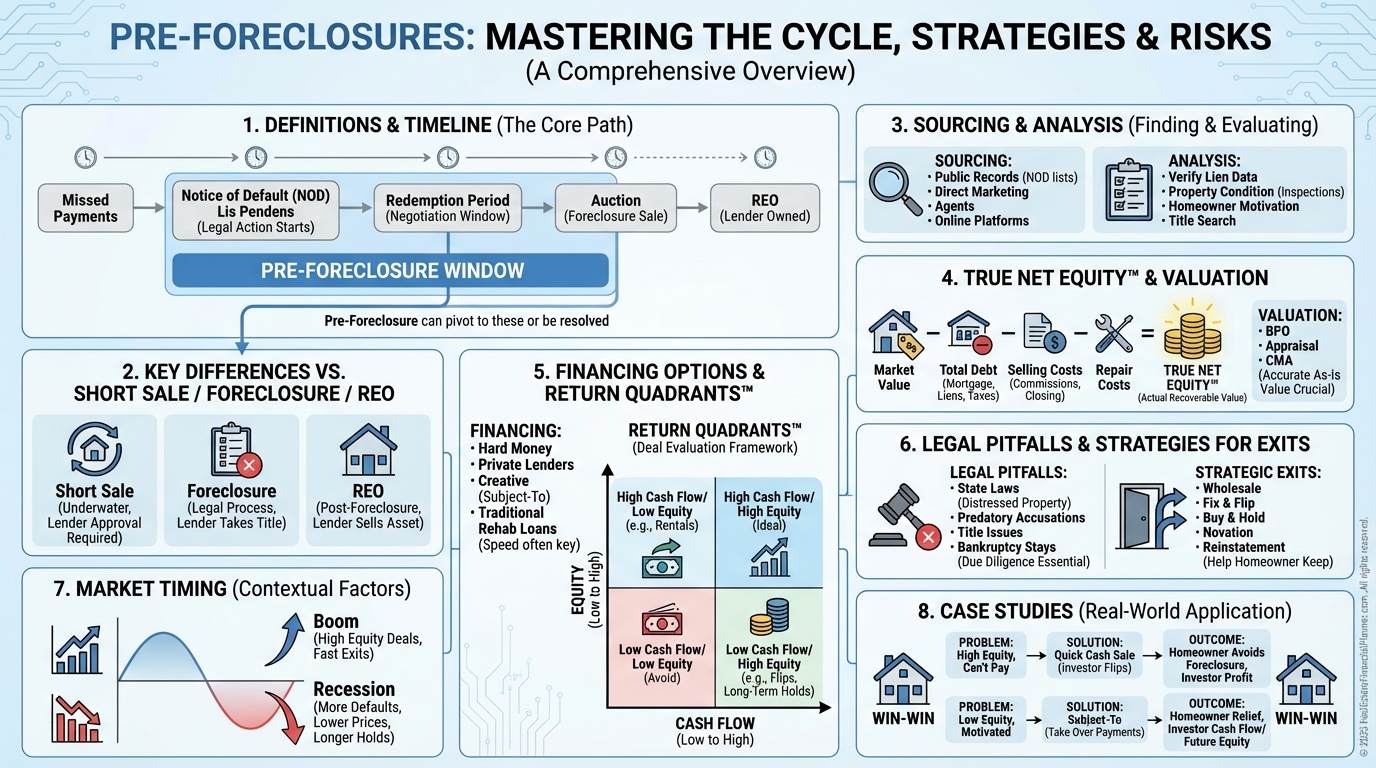

What Pre-Foreclosures Actually Are

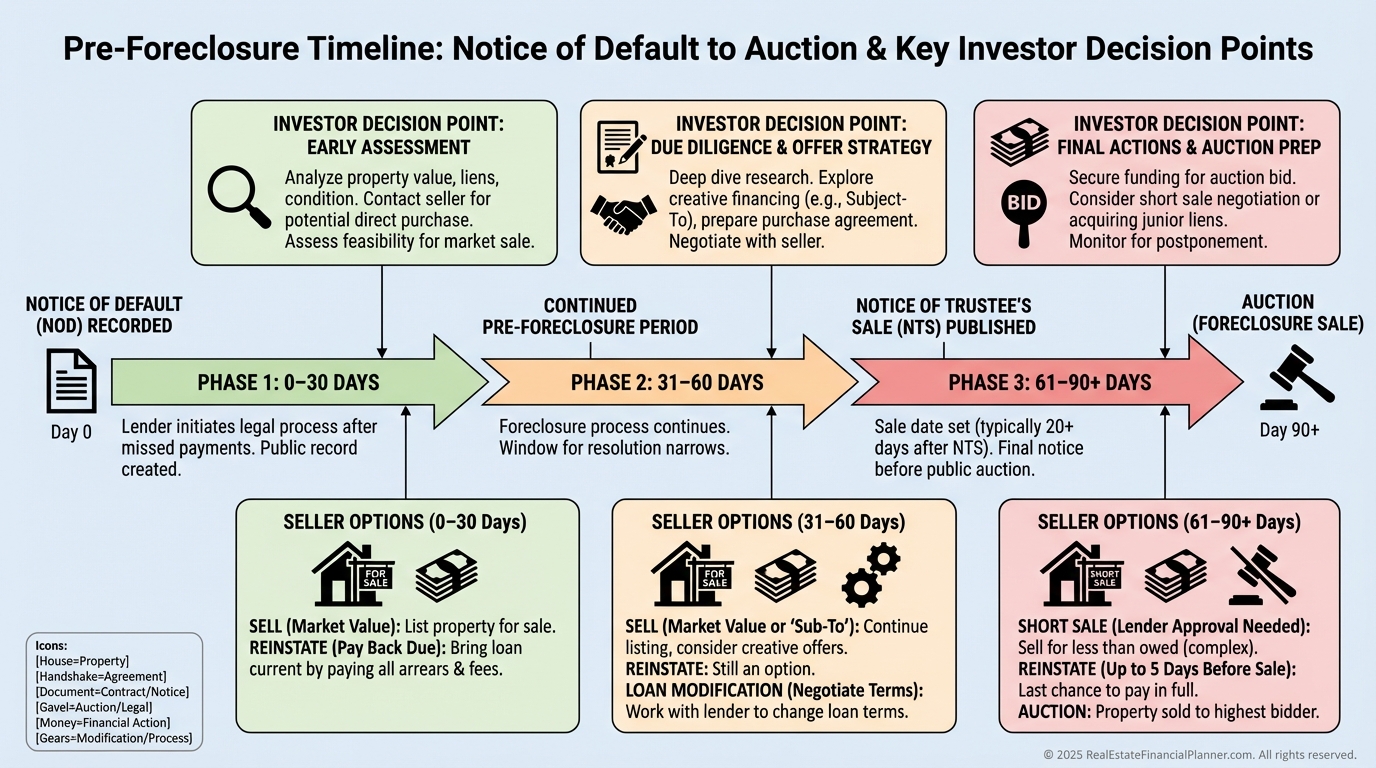

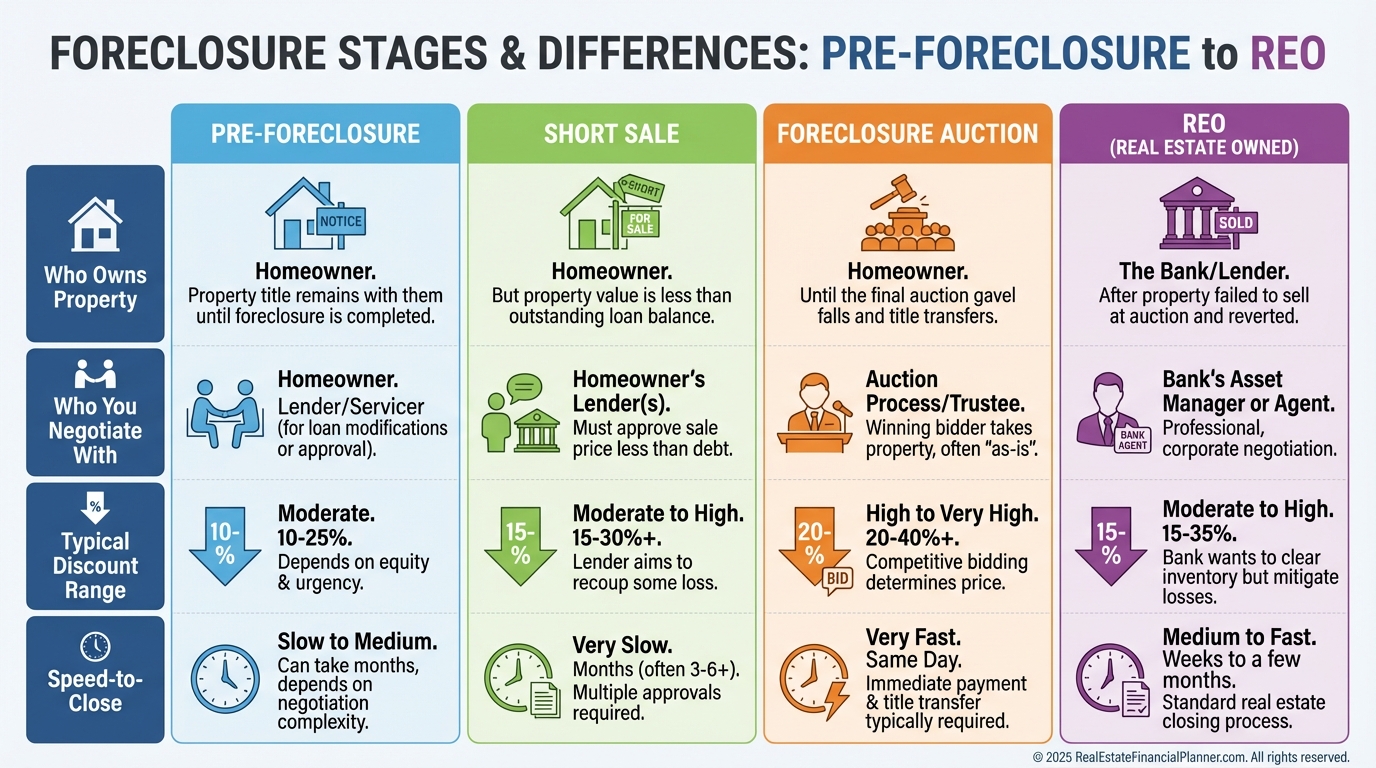

A pre-foreclosure begins when the lender records a Notice of Default and ends when the property goes to auction.

During this window, the owner still owns the property and can sell, rent, refinance, or negotiate.

In most states, this window runs 90–120 days.

Some judicial states stretch longer, which increases your planning runway.

The legal status is simple but critical.

The seller can transfer clear title just like any other sale, as long as liens and arrears are paid at closing.

Urgency is real, but the transaction is normal.

How It Differs From Related Terms

In pre-foreclosure, you negotiate directly with the homeowner.

In foreclosure or REO, you negotiate with a lender or asset manager after the auction.

A short sale only occurs if the debt exceeds value and the bank agrees to accept less.

Plenty of pre-foreclosures have equity and never become short sales.

REOs are post-foreclosure and often hit the MLS closer to market price.

Pre-foreclosures trade for less because you solve a time-sensitive problem for the owner.

How Discounts Show Up in Your Numbers

Time pressure and condition issues create discounts.

That’s your margin.

I model three things with clients before they write offers.

A 20–30% discount to ARV builds instant equity.

A lower purchase price improves cap rate without changing rents.

Every $10,000 you don’t spend saves roughly $50–$75 per month in debt service, depending on terms.

We verify with The World’s Greatest Real Estate Deal Analysis Spreadsheet™ and then stress test.

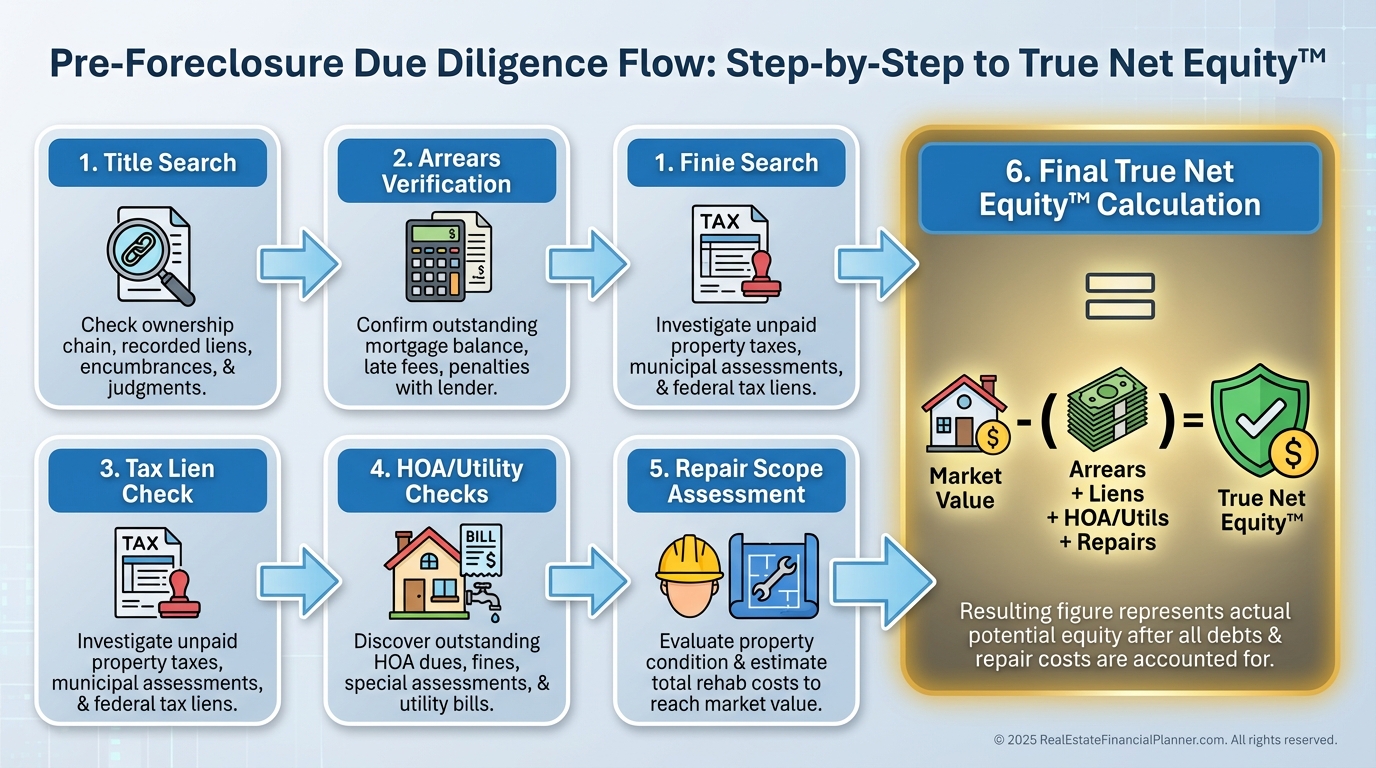

The REFP Lens: True Net Equity™ and Return Quadrants™

Gross equity is not your equity.

True Net Equity™ is what remains after purchase credits, arrears, closing costs, fees, repairs, and selling costs if you needed to exit.

I don’t greenlight a deal until True Net Equity™ is clearly positive with a margin of safety.

Then we look at the Return Quadrants™.

A pre-foreclosure discount typically boosts three quadrants on day one.

That’s why these look like “home runs” when analyzed correctly.

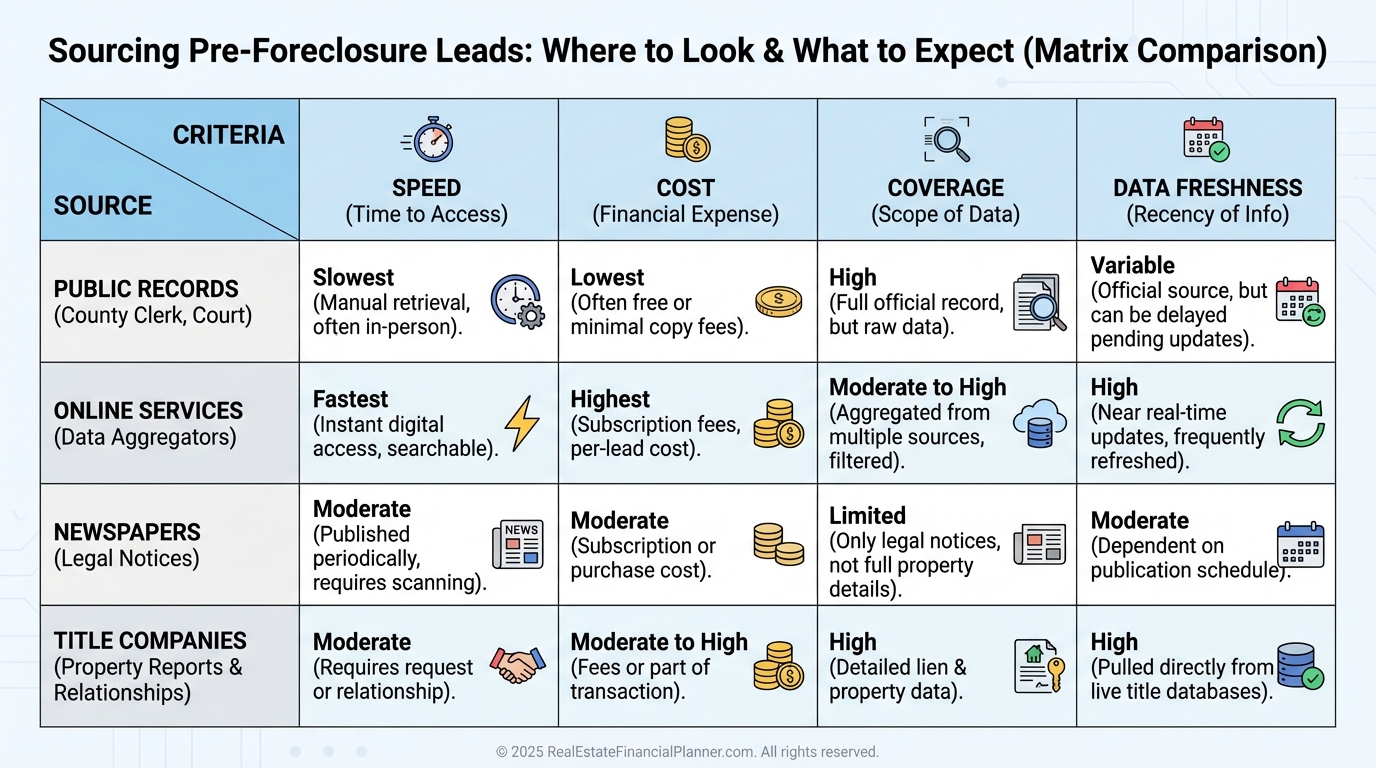

Finding Quality Pre-Foreclosure Leads

I tell new investors to start where pros do.

Public records are free and early.

Online aggregators save time if your market is large.

Title reps help if you already close deals.

Local legal notices still work in smaller towns.

I batch leads weekly and assign statuses: new, contacted, follow-up, meeting, offer, under contract.

Speed matters, but organization wins.

How I Analyze a Pre-Foreclosure in 12 Minutes

First, I confirm value with tight comps.

Then I pull open liens to estimate equity.

I check the NOD date to gauge urgency.

I scan for code violations and utility shutoffs to infer condition.

If equity is 20%+ and timeline is inside 60 days, I escalate to a conversation.

If equity is thin, I consider short sale mechanics or pass.

Due Diligence That Protects Your Profit

Title work reveals junior liens and judgments.

You must verify arrears and reinstatement with the lender’s loss mitigation team.

I always confirm property tax status because tax liens can jump the line.

HOA arrears and special assessments can be silent killers.

If I discover surprises, I rework the price or I walk.

Example: The Duplex That Paid for Itself

A client, Marcus, spotted a duplex with comps at $300,000.

The first mortgage balance was $220,000 with no seconds.

We confirmed $80,000 of gross equity and about $11,500 in arrears, fees, and costs.

He offered $250,000, leaving the seller $30,000 after paying arrears and closing.

That preserved dignity for the owner and left Marcus with ~$50,000 in True Net Equity™ on day one.

He closed in 12 days with hard money, refinanced at six months, and kept it as a cash-flowing rental.

Valuation Realities in Distressed Situations

Pre-foreclosure pricing trades on urgency.

Closer to auction, discounts widen.

Condition is usually “as-is,” so I budget 1.5–2x the visible repair list to catch the hidden items.

I’d rather be pleasantly surprised than undercapitalized.

If the discount doesn’t cover repair uncertainty, I don’t force it.

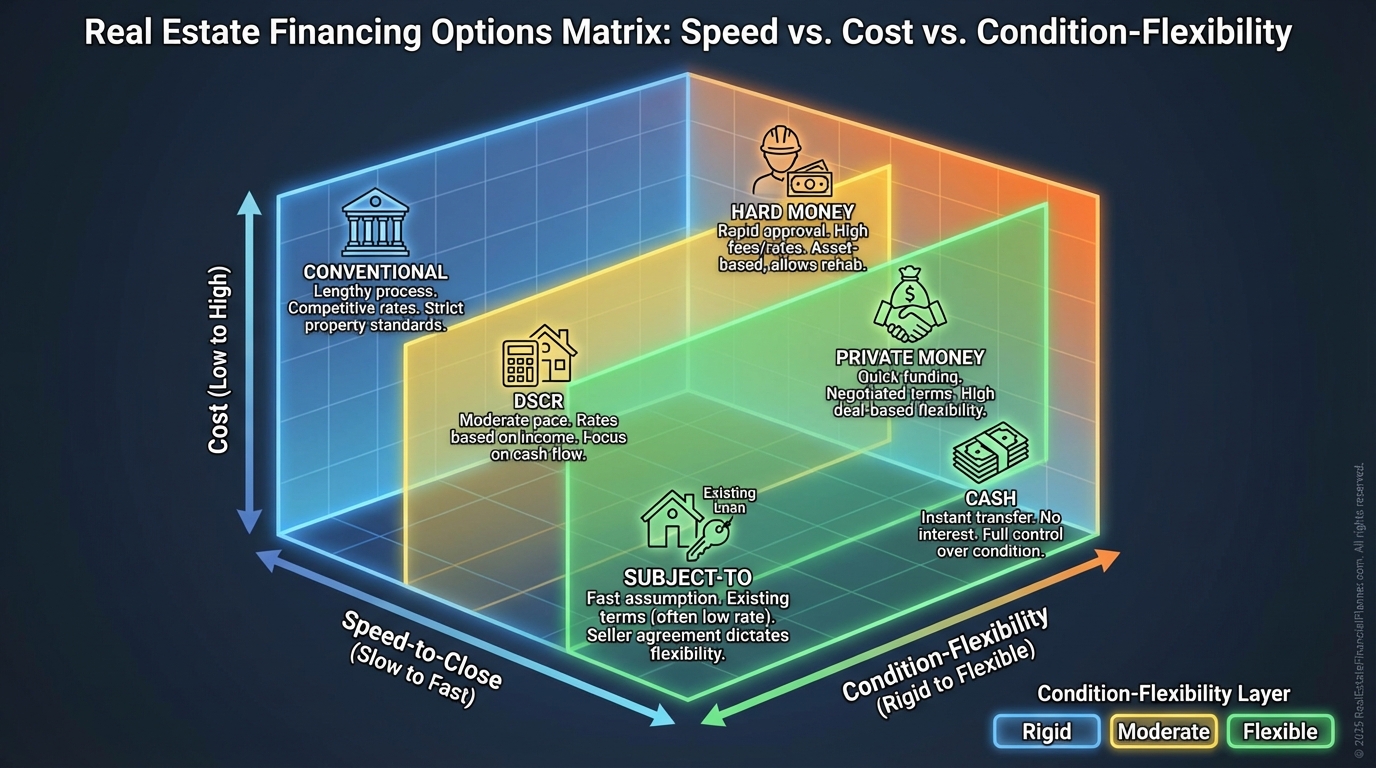

Financing That Matches the Clock

Traditional mortgages often can’t move fast enough.

Hard money and private money exist to fill that gap.

Yes, the rates are higher.

No, it doesn’t matter if you’re buying 20%–30% below value and turning quickly.

Subject-to can work when the existing loan is attractive and you structure it with competent counsel.

Cash is king when the seller’s fear is the calendar.

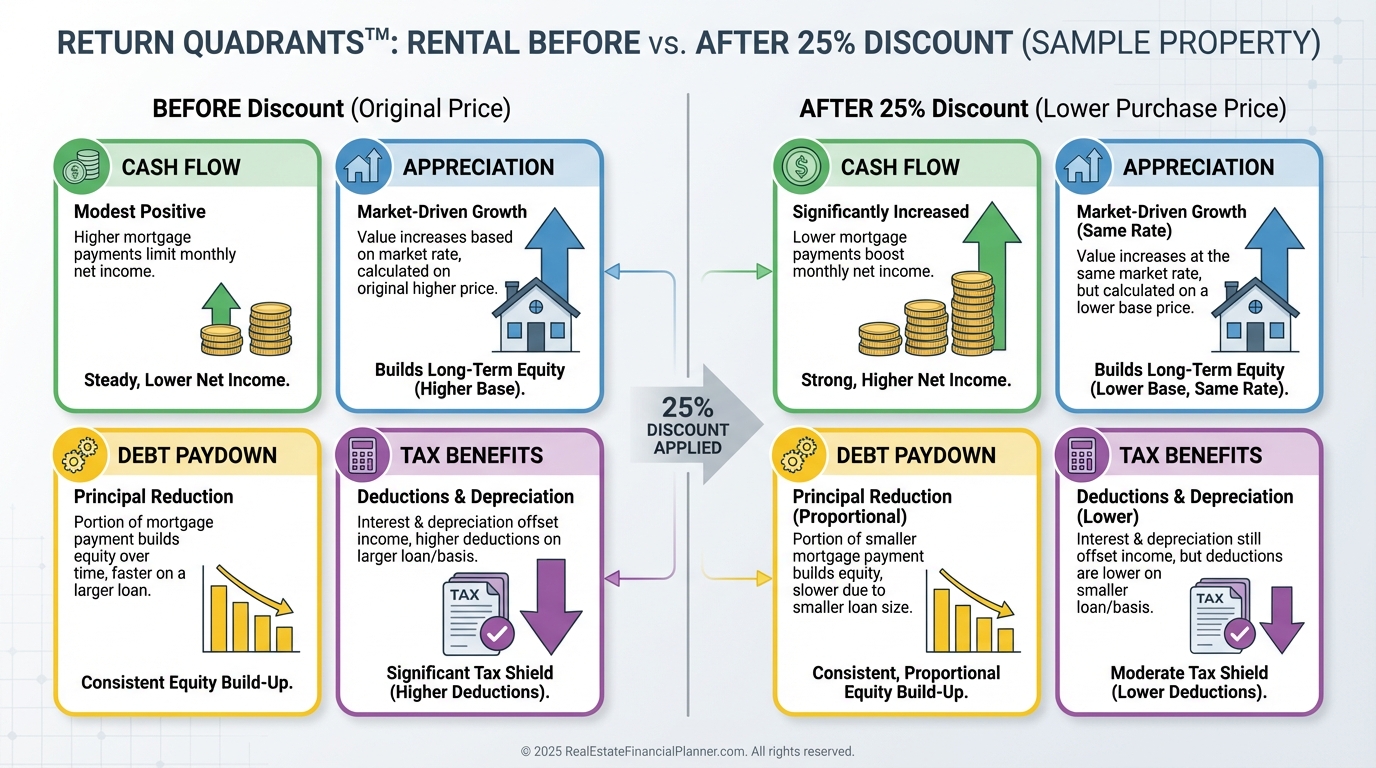

Modeling Returns the Right Way

I run Return Quadrants™ before and after the discount to see where the lift shows up.

Cash flow improves from a lower basis and sometimes better LTV on refinance.

Debt paydown is unchanged per dollar borrowed, but you’ve borrowed fewer dollars.

Appreciation is on market value, not your cost, so your equity compounds faster.

Tax benefits are the same property, but your yield on cash invested increases.

We validate with The World’s Greatest Real Estate Deal Analysis Spreadsheet™ and sensitivity-test exit timelines.

Common Mistakes I See (And Stop)

Assuming every pre-foreclosure is underwater.

Plenty have equity but no liquidity.

Waiting until the week before auction.

You lose leverage and invite chaos.

Skipping lien checks because the seller “thinks” balances are lower.

The meter is running, and estimates are usually wrong.

Underestimating repairs because the house “looks fine from the street.”

Distress hides inside walls, crawlspaces, and panels.

Communication and Compliance

You are helping a person in crisis.

Lead with empathy and clear options.

I put everything in writing and never promise what I can’t control.

Some states regulate pre-foreclosure solicitations, cooling-off periods, and disclosures.

I have local counsel review my documents before I scale.

You should too.

Strategy: Using Pre-Foreclosures to Build a Portfolio

Buy-and-hold becomes safer with instant equity.

It accelerates the flywheel when you refinance at stabilized value.

Value-add is where you get paid for competence, not speculation.

I target cosmetic-heavy, structural-light projects for best risk-adjusted returns.

You can even use Nomad™ in select cases.

Owner-occupants who can close quickly and move in for a year may unlock favorable financing and live-in rehab efficiencies.

Exit Plans That Fit the Deal

Wholesale if you control a deep discount and need speed.

Fix-and-flip if the scope is tight and comps are clear.

Keep as a rental if the stabilized numbers sing and the neighborhood is improving.

Seller financing is an elegant solution when you can help the owner avoid foreclosure and create terms that cash flow.

Market Timing: Where to Point the Ship

Foreclosure filings, unemployment trends, and transaction volume tell you where the puck is headed.

I allocate more time to pre-foreclosures when filings rise and competition falls.

Seasonally, January and September spikes are real.

Line up capital in December and August, then work your plan.

Case Study: From One Deal to Twelve

Jennifer started with $40,000 and a clear buy box.

Her first pre-foreclosure was worth $220,000 with $60,000 equity and $8,000 in arrears.

She paid $180,000, put $25,000 into cosmetics, rented it, and refinanced at $245,000.

Her cash came back plus an extra $20,000 for the next deal.

She repeated the cycle every 4–6 months.

Three years later she held 12 units, $5,000/month in cash flow, and over $400,000 in equity.

That wasn’t luck.

It was a system.

Your First Week Action Plan

Pull the last 7–14 days of NODs.

Pick a tight buy box and run True Net Equity™ on five addresses.

Call loss mitigation to verify arrears on the best two.

Prepare funds: hard money approval, private money conversations, or cash.

Knock politely, listen first, and present solutions that preserve the seller’s dignity.

Do the right deal, not every deal.

Final Thought

Pre-foreclosures reward investors who respect the clock, the seller, and the math.

When you pair empathy with disciplined analysis, you create win-win transactions and durable wealth.